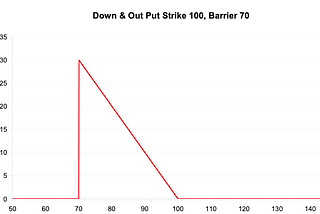

Andrea ChelloinThe Quant JourneyPricing Barrier Options using Monte Carlo SimulationBarrier options are options that have a payout that is dependent on the terminal stock price and whether or not they reach a barrierMay 17, 2022May 17, 2022

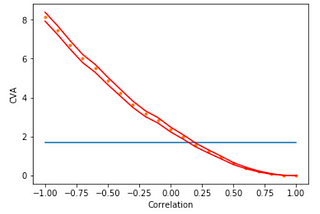

Andrea ChelloinThe Quant JourneyMonte Carlo Methods for Risk Management: CVA and the Merton Model in PythonCVA is the difference between the value of a portfolio which we assume is risk-free, and a portfolio where we account for default riskMay 16, 2022May 16, 2022

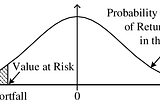

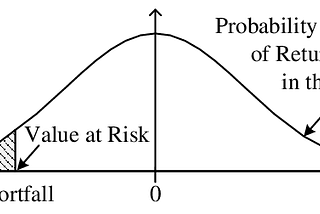

Andrea ChelloinThe Quant JourneyMonte Carlo Methods for Risk Management: VaR Estimation in PythonValue at Risk gives an indication of how much you stand to lose on a portfolio with a given probability, over a specific time period.May 16, 20221May 16, 20221

Andrea ChelloinThe Quant JourneyMonte Carlo Simulation for Black-Scholes Option PricingIn this article we will look at applying Monte Carlo simulation to price both a European Call and Put Option, following the Black-Scholes…Apr 24, 20222Apr 24, 20222

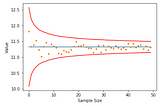

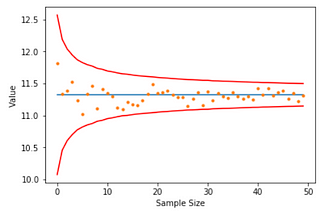

Andrea ChelloinThe Quant JourneyMonte Carlo Simulation Theory and Applications in PythonThe Monte Carlo Simulation is a numerical analysis technique aimed at estimating the possible outcomes of a certain random event. It is a…Apr 23, 2022Apr 23, 2022

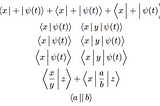

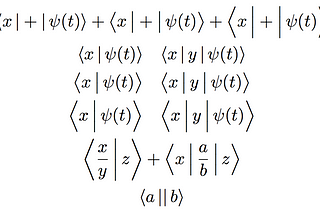

Andrea ChelloinThe Quant JourneyComprehensive Guide to The Mathematics of Quantum MechanicsThe mathematical formulations of quantum mechanics are those mathematical formalisms that permit a rigorous description of quantum…Feb 19, 20222Feb 19, 20222

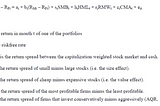

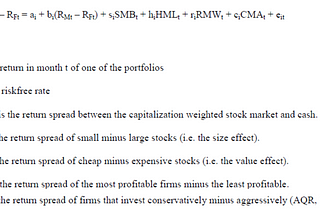

Andrea ChelloinThe Quant JourneyFive-Factor Asset Pricing Model AnalysisA Regression based analysis of the Five-Factor Asset Pricing ModelFeb 17, 2022Feb 17, 2022

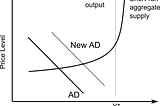

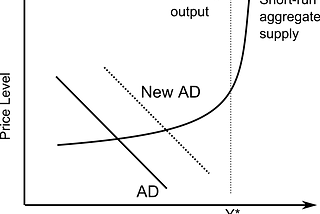

Andrea ChelloinThe Quant JourneyEffects of Changes in Oil Rents and Broad Money on an AS-AD Model from 1970 to 2007Using data from a set of 5 different countries graph the effects of changes in Oil rents and Broad money on an AS-AD Model starting at…Feb 16, 2022Feb 16, 2022

Andrea ChelloinThe Quant JourneyThe Global Financial Crisis of 2008: Regulations Explained ComputationallyDissecting the most impactful financial crisis in history, how monetary policy influenced the recovery from the crisis, and analyzing…Feb 16, 20221Feb 16, 20221

Andrea ChelloinThe Quant JourneyHedge Fund Failures: A Computational Analysis of the Sources of RiskIt is imperative to understand the role of Hedge Funds in the financial sector today, and how they have, over time, played significant…Feb 16, 2022Feb 16, 2022